Key Takeaways

- →Pre-seed, seed, and Series A aren't just bigger checks — each stage funds a different question: can the idea exist, can it grow, can it scale.

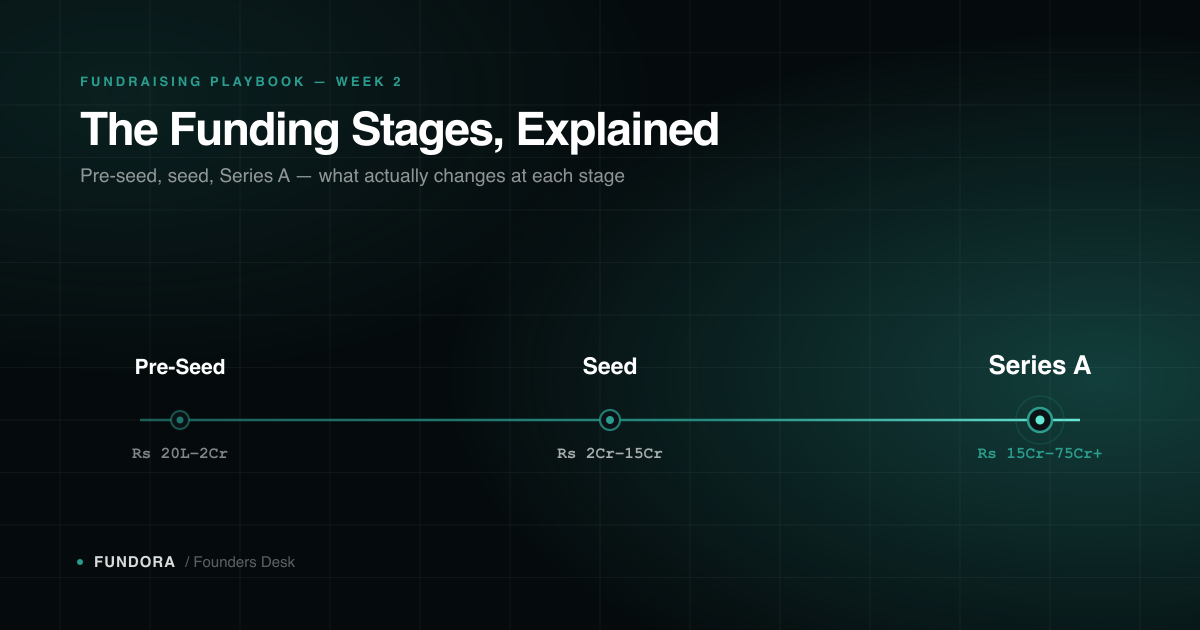

- →Indian check sizes roughly track ₹20L–₹2Cr at pre-seed, ₹2Cr–₹15Cr at seed, and ₹15Cr–₹75Cr+ at Series A, though ranges vary by sector.

- →The most common first-raise mistake is pitching the wrong stage's evidence — Series A-style metrics at seed, or seed-style vision at Series A.

Pre-seed, seed, and Series A get talked about as if they're just checkpoints on a size chart — bigger round, bigger number, next stage. They're not. Each stage exists because investors are trying to answer a different question about your company, and pitching the wrong question's evidence is one of the most common reasons a strong company gets a confused response from the wrong-stage investor. This is Week 2 of Fundora's Fundraising Playbook series, and it breaks down what actually changes at each stage — not just the check size.

#Pre-Seed — Proving The Idea Can Exist

Pre-seed is the earliest stage — usually before a product is fully built, and sometimes before there's any revenue at all. Money at this stage typically comes from a founder's own savings, friends and family, or angel investors; institutional VCs are rarely writing pre-seed checks. What's actually being funded isn't a business model — it's a founder's ability to build a first version and find early signals that someone wants it. Typical amounts in India run roughly ₹20L–₹2Cr, though this varies widely by sector.

At this stage, investors are betting almost entirely on the founder and the problem — there's rarely enough product or data to bet on anything else.

#Seed — Proving The Idea Can Grow

By seed, the company usually has a working product and some early users or revenue, even if small. Money now comes from seed funds, angel networks, and micro-VCs — the first "professional" money for many founders. What's actually being funded is turning early signal into a repeatable pattern: enough evidence that the pre-seed traction wasn't a fluke. Typical amounts in India run roughly ₹2Cr–₹15Cr.

This is usually the first round where investors expect an actual pitch deck, basic metrics, and a real go-to-market plan — not just a founder story.

#Series A — Proving The Idea Can Scale

At Series A, the company has found a working model — real product-market fit signals — and now needs capital to grow it faster. Money comes from institutional VCs writing much larger checks. What's actually being funded is scaling what's already working: more team, more markets, more distribution. Typical amounts in India run roughly ₹15Cr–₹75Cr+.

The bar shifts here — from "does this have potential" to "does the data prove this works." Vague enthusiasm stops being enough.

Each stage isn't just a bigger check — it's a different question the investor is trying to answer. Understanding which question you're being asked is the difference between a strong pitch and a mismatched one.

#Comparing The Stages At A Glance

| Stage | What's Being Proven | Typical Indian Check Size | Typical Investor Type | What Investors Look For |

|---|---|---|---|---|

| Pre-Seed | The idea can exist — a first version can be built and someone wants it | ₹20L–₹2Cr | Founders' savings, friends & family, angel investors | A credible founder and a real, specific problem |

| Seed | The idea can grow — early signal turns into a repeatable pattern | ₹2Cr–₹15Cr | Seed funds, angel networks, micro-VCs | A pitch deck, basic metrics, and a real go-to-market plan |

| Series A | The idea can scale — a working model can grow faster with more capital | ₹15Cr–₹75Cr+ | Institutional VCs | Data that proves the model works, not just potential |

#How To Know Which Stage You're Actually At

Founders often anchor on time elapsed — "we've been at this for a year, we must be seed by now." Stage isn't a function of how long you've been working. It's a function of product status and revenue. A simple self-check:

- ✓No live product yet, or a rough first version only you and a few testers have used — you're pre-seed, regardless of how many months you've been building.

- ✓A working product with real, if small, usage or revenue that showed up without you personally chasing every user — you're likely at seed.

- ✓Consistent revenue growth, a repeatable way customers find you, and a model that mainly needs more fuel to grow faster — you're approaching Series A.

- ✓If you're genuinely unsure between two stages, default to the earlier one. Undershooting gets you a fast, comfortable yes from the right investor; overshooting gets you a slower, harder no from the wrong one.

#Why This Matters For Your First Raise

The most common mistake at this point isn't a bad pitch — it's a mismatched one. A seed-stage founder who shows up with a Series A-style data room, elaborate growth projections, and no clear founder-market story is answering a question no one asked yet; a seed investor wants to know if the early signal is real, not whether the five-year model is airtight. The reverse mistake is just as common: a Series A founder who leans on vision and founder narrative the way they did at seed, without the metrics to back it, runs into investors who have already moved past "does this have potential" and are now asking "does the data prove this works." Knowing which of the three questions above your company is actually being asked — before you write the deck — is what makes a raise feel obvious instead of like a mismatch you have to talk your way around.

Fundraising Playbook Series

This is Week 2 of Fundora's Fundraising Playbook. Week 3 will look at what actually happens once you've picked a stage and start building the pitch itself — coming soon.

Find your right investors on Fundora

Build a verified profile and get AI-matched to investors who fit your stage, sector, and ticket size.