Key Takeaways

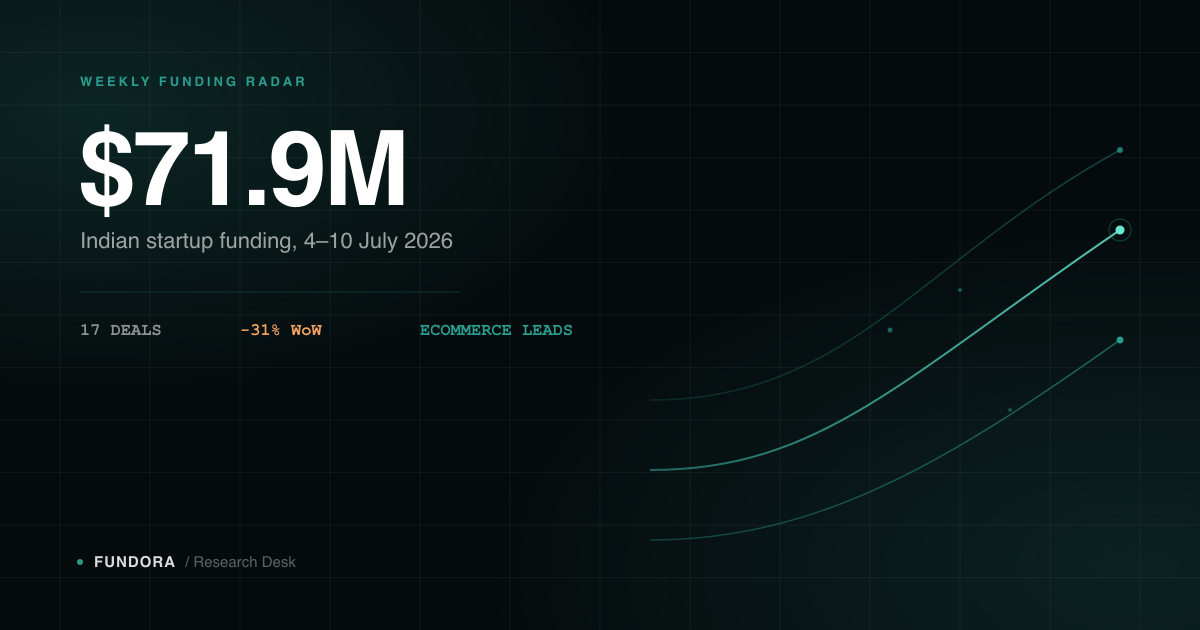

- →Indian startups raised $71.9M across 17 disclosed deals for the week of July 4–10, 2026, down 31% from the prior week's $104.6M — a decline in deal count and size, not one outlier unwinding.

- →Debt financing accounted for $27M (37.6%) of the week's total, driven by two D2C ecommerce companies — a debt-heavy week that typically signals working-capital raises rather than growth-equity conviction.

- →Ecommerce led sector funding for a second consecutive week, this time spread across 7 deals rather than concentrated in one outlier round — a structurally healthier signal than single-round sector spikes.

Indian startups raised $71.9M across 17 disclosed deals in the week ending 10 July 2026, according to Inc42 deal data — down 31% from the $104.6M recorded the prior week. Unlike the prior two weeks, where a single mega-round distorted the headline number, this decline shows up in deal count and average deal size both. Here's the breakdown, sector by sector, stage by stage.

#This Week's Funding Breakdown

The week's largest deal was Elevate Education's $17.7M Series D, led by WestBridge Capital — an edtech round, not the ecommerce or fintech names that typically top the weekly list. Two debt rounds in D2C ecommerce, Purple Style Labs' $17M and Aukera's $10M, followed close behind. Below the top three, the remaining 14 deals ranged from a $8.5M agritech round down to sub-$500K pre-seed checks.

| Rank | Company | Amount | Sector | Stage | Lead Investor |

|---|---|---|---|---|---|

| 1 | Elevate Education | $17.7M | Edtech | Series D | WestBridge Capital |

| 2 | Purple Style Labs | $17M | Ecommerce (D2C) | Debt | Kairos Ventures |

| 3 | Aukera | $10M | Ecommerce (D2C) | Debt | Alteria Capital |

| 4 | Wheelocity | $8.5M | Agritech | Undisclosed | Elevar Equity |

| 5 | Econovus Packaging | $4.2M | Logistics | Pre-Series A | Rainmatter |

| 6 | thumpN | $3.8M | Media & Entertainment | Pre-Seed | Madhur Deora, Arijit Singh, Sunidhi Chauhan, Badshah |

| 7 | Mowito | $3M | Advanced IoT & Hardware | Pre-Seed | Version One Ventures |

| 8 | Milo Drive | $2.4M | Travel Tech | Seed | Caret Capital, Antler |

| 9 | The Func Labs | $1.5M | Ecommerce (D2C) | Seed | Nisaba Godrej, Anand Piramal |

| 10 | Doodhvale Farms | $1M | Ecommerce (D2C) | Undisclosed | Atomic Capital |

| 11 | Stylework | $1M | Real Estate Tech | Pre-Series B | Auxano Capital |

| 12 | Neothera | $943K | Ecommerce (D2C) | Undisclosed | Blume Ventures |

| 13 | BAAS Technologies | $525K | Advanced IoT & Hardware | Pre-Seed | Inflection Point Ventures |

| 14 | Avni Wellness | $419K | Health Tech | Undisclosed | Proteus Partners |

| 15 | Fizzy Goblet | Undisclosed | Ecommerce (D2C) | Undisclosed | Kareena Kapoor Khan (angel) |

| 16 | Rawbare | Undisclosed | Ecommerce (D2C) | Undisclosed | Teamology Softech |

| 17 | Rocketlane | Undisclosed | AI (Application Layer) | Undisclosed | Atlassian Ventures |

14 Disclosed-Amount Deals This Week ($M)

Chart excludes Fizzy Goblet, Rawbare, and Rocketlane — all three closed rounds this week without disclosing an amount. They're included in the 17-deal count and in sector/stage deal counts, but not in any dollar total or ranking on this page.

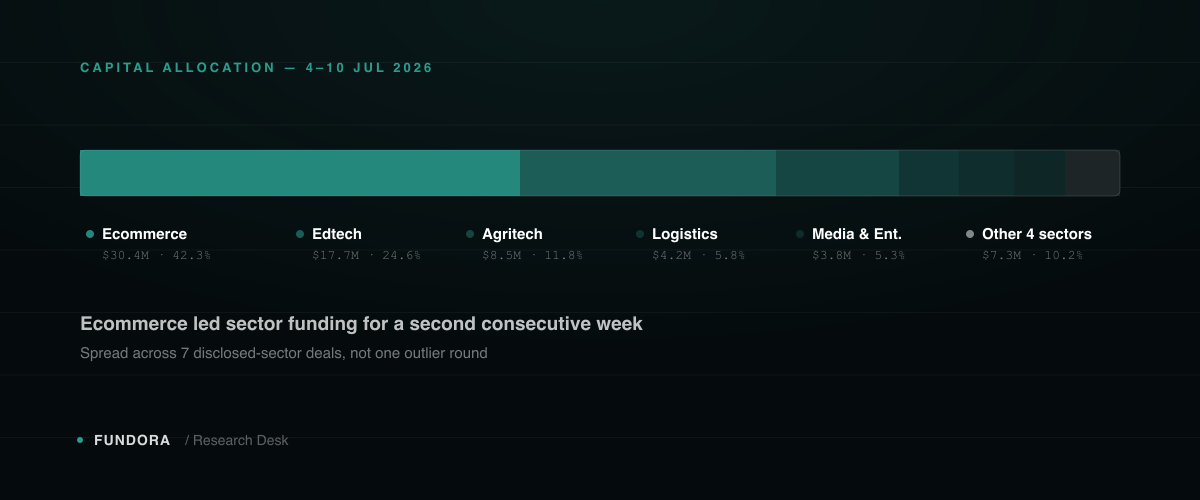

#Capital By Sector

Ecommerce was the top-funded sector for the second consecutive week, led by Purple Style Labs' $17M debt round — the largest cheque in the segment. Inc42's own weekly aggregate puts Ecommerce at roughly $28.9M across 6 deals; Fundora's full reconciliation below adds The Func Labs' $1.5M seed round, which is tagged Ecommerce (D2C) in this week's disclosed deal list but appears to be counted separately in Inc42's early-stage highlights rather than folded into their sector total. Including it, Ecommerce's disclosed total for the week is $30.4M across 7 deals.

Capital by Sector ($M)

Donut chart shows disclosed-amount sectors only. AI (Rocketlane's round, amount undisclosed) is excluded from the chart but appears in the sector table below with its deal count.

Sector Summary

| Sector | Amount | % Share | Deal Count |

|---|---|---|---|

| Ecommerce | $30.4M | 42.3% | 7 |

| Edtech | $17.7M | 24.6% | 1 |

| Agritech | $8.5M | 11.8% | 1 |

| Logistics | $4.2M | 5.8% | 1 |

| Media & Entertainment | $3.8M | 5.3% | 1 |

| Advanced IoT & Hardware | $3.5M | 4.9% | 2 |

| Travel Tech | $2.4M | 3.3% | 1 |

| Real Estate Tech | $1.0M | 1.4% | 1 |

| Health Tech | $0.4M | 0.6% | 1 |

| AI | Undisclosed | — | 1 |

Figures are rounded to the nearest $0.1M and nearest 0.1 percentage point, so column totals may not sum to exactly $71.9M or 100% — this is a rounding artifact, not a data gap. Ecommerce's $30.4M / 7-deal figure is Fundora's reconciliation of the full disclosed deal list; where this page cites Inc42's own headline sector number, it uses their published $28.9M / 6 deals instead. Both are accurate under their respective methodologies and are called out explicitly wherever they appear.

#Capital By Stage

The stage breakdown is where this week's real story sits. Debt — not equity — was the largest single financing instrument of the week, ahead of Series D and every early-stage equity stage combined.

Capital by Stage ($M)

Stage Summary

| Stage | Amount | % Share | Deal Count |

|---|---|---|---|

| Debt | $27.0M | 37.6% | 2 |

| Series D | $17.7M | 24.6% | 1 |

| Undisclosed stage | $10.9M | 15.1% | 7 |

| Pre-Seed | $7.3M | 10.2% | 3 |

| Pre-Series A | $4.2M | 5.8% | 1 |

| Seed | $3.9M | 5.4% | 2 |

| Pre-Series B | $1.0M | 1.4% | 1 |

Of the 7 "undisclosed stage" deals, 4 disclosed an amount without a named stage (Wheelocity, Doodhvale Farms, Neothera, Avni Wellness — $10.9M combined) and 3 disclosed neither stage nor amount (Fizzy Goblet, Rawbare, Rocketlane — excluded from every dollar figure on this page, included in every deal count).

$27M of this week's $71.9M — 37.6% — came from debt, not equity. Two D2C ecommerce companies account for all of it.

#What Fundora Sees

Ecommerce's win looks structurally different this time

Two weeks ago, sector "wins" in this data were almost entirely a function of one outlier round — AI's 62% share of that week's capital came almost entirely from Sarvam's single round, not from broad-based deal flow. This week's Ecommerce lead is the opposite pattern: 7 separate companies, ranging from a $17M debt round down to a $943K raise, rather than one company distorting the whole sector's number. Distributed strength across many independent cap tables is a more durable signal of sector demand than a total propped up by a single check, because it doesn't unwind the moment one fund or one company's round gets delayed.

A debt-heavy week is a different signal than an equity-heavy one

Purple Style Labs and Aukera together raised $27M in debt this week — more capital than any single equity stage, including the week's largest Series D. Debt financing and equity financing answer different questions for a company. An equity round is a bet on a company's future value; a debt round, particularly for D2C and ecommerce businesses with predictable revenue, is typically financing working capital — inventory, logistics, marketing spend against known unit economics — not underwriting the company's long-term thesis. A week where debt outweighs every equity stage isn't evidence of stronger or weaker investor conviction in Indian ecommerce; it's evidence that more of this week's ecommerce capital came from lenders extending credit against revenue than from investors buying equity against a growth story. Both are legitimate financing paths, but conflating the two when reading "capital raised" headlines overstates how much of this week's total reflects growth-stage equity appetite.

Early-stage capital: thin, but not thinner than it looks

Pre-seed and seed rounds combined for $11.2M across 5 deals this week, led by thumpN's $3.8M pre-seed and Mowito's $3M pre-seed. That's close in dollar terms to last week's seed-stage total alone — $11.2M across 5 deals, as covered in Fundora's prior Funding Radar — but this week's figure spans both pre-seed and seed combined, and last week additionally saw $1.9M across 4 separate pre-seed deals on top of that. In other words, early-stage deal count roughly halved week over week even as the early-stage dollar total held close to flat, because two unusually large pre-seed checks (thumpN, Mowito) did more work per round than the broader spread of smaller checks seen the prior week. One week of thinner early-stage deal flow isn't a trend on its own, but it's worth watching alongside next week's numbers.

Total Weekly Funding — 3-Week Trend ($M)

*The week ending 27 June's raw total was $1.12B, but $900M of that was CRED's single Series H round. The chart above uses the outlier-adjusted ~$220M figure from that period, consistent with how Fundora's prior Funding Radar treated the same outlier, so that three genuinely comparable weeks sit on one readable scale. On that basis, total weekly funding has now declined for two straight weeks — $220M to $104.6M to $71.9M — though 3 data points is still a short window to call a trend rather than normal week-to-week variance.

#Beyond The Funding Numbers

Two new funds launched this week, per Inc42: Fundamentum Partnership closed a ₹2,200 Cr third fund led by Nandan Nilekani and Sanjeev Aggarwal, targeting consumer tech, fintech, and AI, while Next Bharat Ventures launched a ₹2,000 Cr second impact fund targeting healthcare, fintech, agritech, and cleantech. Separately, several companies advanced toward public markets this week — Cult.fit filed its DRHP, CarDekho filed draft papers, C5i made a confidential filing, and RentoMojo received SEBI clearance. Fresh fund closes and multiple simultaneous IPO filings suggest continued confidence at the top of the market even as this week's early and growth-stage deal funding cooled.

#What This Means For Founders

If you're a D2C or ecommerce founder with a revenue history, this week is a reminder that debt is an active, real financing channel right now — not a fallback for companies that couldn't raise equity. It's worth modeling alongside a priced round, particularly for working-capital-intensive spend like inventory and logistics, rather than defaulting to equity by habit. If you're an early-stage founder, the check sizes this week (three pre-seed rounds from $525K to $3.8M, two seed rounds from $1.5M to $2.4M) show that early capital is still moving, just concentrated in fewer, larger checks than the week before — a reason to be precise about the size of the round you're actually asking for, rather than anchoring to what a similar company raised in a thinner week. And across the board: one week of data, in either direction, is a data point, not a verdict on the market.

Previous Funding Radar

If you're building a D2C or ecommerce brand weighing debt against your next equity round, that's a specific, numbers-driven decision — not a default. Fundora's investor-matching tools cover both lenders and equity investors active in Indian ecommerce right now, so you can compare what each path actually costs before you commit to one.

Find your right investors on Fundora

Build a verified profile and get AI-matched to investors who fit your stage, sector, and ticket size.